Key Takeaways:

- Only 44% of Bitcoin ETF inflows represent genuine long-term investment.

- The Bitcoin ETF trading volumes are significantly influenced by both Arbitrage and carry trade strategies.

- A spike in funding rates can lead to a decrease in hedge fund positioning in the ETF.

Since the launch of spot Bitcoin ETFs in January 2024, they have been widely discussed, attracting billions of dollars in investment. But a closer look shows not all that money is coming in for the long haul. Much of this is being driven by more sophisticated merchant trading strategies, raising the question of whether there is truly demand for Bitcoin as a long-term asset.

Table of Contents

The Bitcoin ETF: Beyond the Headlines

The picture painted around spot Bitcoin ETFs has been one of universal institutional adoption, leading to a massive increase in demand and a coinciding price rise for Bitcoin. But that picture might be incomplete, according to research by 10x Research, under Markus Thielen.

U.S. spot Bitcoin ETFs have taken in close to $39 billion in net inflows since their launch. However, he estimates that just $17.5 billion, or around 44%, represents true long-only buying. The remaining 56%? It’s probably linked to arbitrage strategies, 10x Research said. This isn’t simply a small detail; it alters how we ought to understand the influence of these ETFs.

Understanding the Arbitrage Game

What are these arbitrage strategies exactly? These can be largely considered as part of the “carry trade,” wherein traders take spot Bitcoin by buying through the ETFs and shorting Bitcoin futures at the same time. The goal is to make money off the “basis”, the difference between the spot price and the futures.

According to Markus Thielen, Head of Research at 10x Research, there is a need for a more comprehensive grasp of the dynamics in play in Bitcoin ETF investments.

Markus Thielen, Head of Research at 10x Research

Let’s take a simple example to illustrate this. Do the math — if spot Bitcoin is trading at $65,000 and Bitcoin futures for expiration in one month are trading at $65,500. Example: A trader can go long Bitcoin through a spot ETF at $65000 and open a short Bitcoin futures position at $65500. When the futures contract matures, they take home the $500 difference, less whatever transaction costs. Due to the nature of this trade profiting from the relative pricing between two similar assets, it has very limited directional risk.

The Consequences for Market Demand

Overall, this focus on arbitrage indicates that the actual demand for Bitcoin as a long term store of value in multi asset portfolios is vastly lower than the headlines would have you believe. This is a crucial point. It can be easy to fall into the trap of extrapolating from ETF inflows and take it as a harbinger of a structural change in institutional sentiment towards Bitcoin. But the arbitrage activity tells a more complicated story.

“Rather than reflecting broad-based institutional adoption, the buying and selling of Bitcoin ETFs is primarily driven by funding rates (basis rate opportunities), with many investors focusing on short-term arbitrage rather than long-term capital appreciation,” Thielen continued. It does not, strictly speaking, require belief in Bitcoin’s value in the long term — it is short-term arbitrage based on static price discrepancies. This raises questions of whether this inflow is sustainable.

Who Are the Big Players?

Thielen went on to explain that hedge funds and trading firms are often the largest holders of BlackRock’s IBIT ETF, for example. These are not average retail investors. These firms “specialize in exploiting market inefficiencies and capturing yield spreads,” not taking directional risk on Bitcoin outright. There is nothing inherently wrong with this, but their primary goal is to generate profits through these strategies rather than holding Bitcoin as a long-term asset. The presence of these institutions points to high levels of arbitrage activity.

The Funding Rate Factor

These arbitrage strategies are profitable based on funding rates and basis spreads. When these rates are sufficiently elevated, the carry trade is profitable. However, this starts to change when the funding rates and base spreads compress to levels that no longer warrant establishing new arbitrage positions.

Hedge funds and trading firms — operating on narrow profit margins — will inevitably respond to the changed environment.

When arbitrage opportunities dry up, these firms cease adding inflows to Bitcoin ETFs, and actually unwind existing ones that no longer offer the same lucrative arbitrage opportunities that were prevalent months ago, as Thielen notes. This is where the risk of precariousness in the market comes into play.

The Outflow Effect

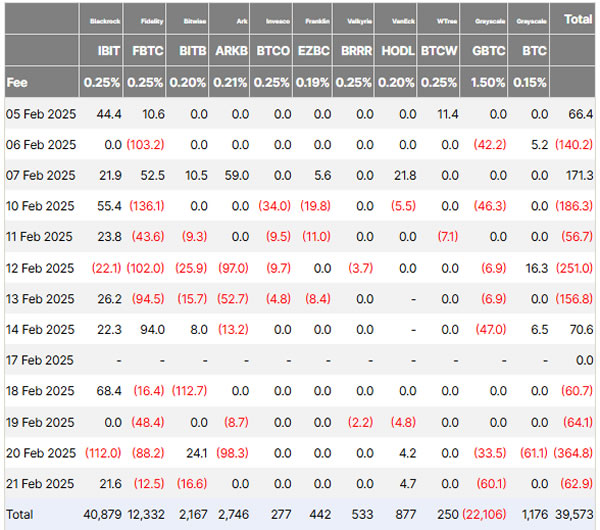

This liquidation of positions can take the form of multiple consecutive days of outflows from Bitcoin ETFs. There were four days of outflows in the week, amounting to $552 million leaving the products, according to Farside Investors. All of this was happening while the price of spot Bitcoin remained within a fairly tight range, signalling that the market impact of such outflows was muted.

Spot Bitcoin ETF flows in February. Source: Farside Investors

But the unwinding process, which marks the initiation of a corrective phase, is, in fact, market-neutral, argues Thielen. This is due to the fact that it means selling ETFs and buying Bitcoin futures, which cancels directional market impact. The objective is to offset both portions of the arbitration trade with little effect on the market price of the underlying Bitcoin.

More News: ETF Flows: Bitcoin and Ethereum Experience Major Sell-Off on February 20

Historical Parallels: Raoul Pal’s Observations

Interestingly, Real Vision CEO Raoul Pal had shared similar thoughts in mid 2024. He estimated that about two-thirds of net inflows into spot Bitcoin ETFs could be attributed to this arbitrage trading. It goes to show that this isn’t a new phenomenon either. Experts knew arbitrage was important in influencing ETF flows for years.

Is the Tide Turning?

While arbitrage remains king, there are early signs that true long-only buying is starting to flow back into the market. Thielen says that real buying flows “have certainly picked up” since the recent US presidential election.

The implication is a possible change of heart. Although arbitrage is still a big driver, it appears that more institutional-style investors who are bullish on Bitcoin for the long-term are playing a role as well. Bitcoin’s price is influenced by external political events and macroeconomic conditions.

This doesn’t mean we should celebrate organic demand prematurely, though.

“While genuine long-only Bitcoin buying has increased since [recent] election, funding rates have collapsed as retail trading volumes have declined.” This dynamic between longer-duration purchases and shorter-term arbitrage will play out in the bitcoin ETF ecosystem.

The reduced funding rates mean the arbitrage strategy is less attractive, and so trading firms have been unwinding their positions over the past week. This highlights the dynamic relationship between ETF inflows/outflows and broader market conditions.

As a result, the Bitcoin ETF market is a complex ecosystem of institutional investment intertwined with profit- and liquidity-providing trading strategies. The market sentiment has changed according to the data, but investors should remain cautious.

Related posts:

US Crypto Index ETFs Face Lukewarm Reception After Launch – What’s Holding Them Back?

US Crypto Index ETFs Face Lukewarm Reception After Launch – What’s Holding Them Back?

ETF Flows: Bitcoin and Ethereum Experience Major Sell-Off on February 20

ETF Flows: Bitcoin and Ethereum Experience Major Sell-Off on February 20

Holding LST 2.0 Tokens to Get Real-World Products and Services

Holding LST 2.0 Tokens to Get Real-World Products and Services

Litecoin Booms: 243% Jump in Transactions as ETF Rumors Swirl

Litecoin Booms: 243% Jump in Transactions as ETF Rumors Swirl

Is the Bitcoin Korea Premium Index Showing Korea Buying Altcoins Instead of Bitcoin?

Is the Bitcoin Korea Premium Index Showing Korea Buying Altcoins Instead of Bitcoin?

Over the past year alone, more than $21 billion has flowed out of the Grayscale Bitcoin Trust ETF

Bitcoin ETF Craze: Demand Surpasses Mining Supply by 3x

BlackRock to Launch Bitcoin ETP in Switzerland for Europe after US ETF Success

Over the past year alone, more than $21 billion has flowed out of the Grayscale Bitcoin Trust ETF

Bitcoin ETF Craze: Demand Surpasses Mining Supply by 3x

BlackRock to Launch Bitcoin ETP in Switzerland for Europe after US ETF Success

Goldman Sachs “U-Turn”: Massive Increase in Bitcoin and Ethereum ETF Investments – A Crypto Market Signal?

Bitcoin DeFi Explodes: TVL Surges 2,000% in 2024 Fueled by Staking and ETFs

Grayscale’s Dogecoin Trust & 21Shares Polkadot ETF Signal New Era for Altcoins

Crypto.com Sets Ambitious Course: Cronos ETF and Stablecoin Launch in 2025

Goldman Sachs “U-Turn”: Massive Increase in Bitcoin and Ethereum ETF Investments – A Crypto Market Signal?

Bitcoin DeFi Explodes: TVL Surges 2,000% in 2024 Fueled by Staking and ETFs

Grayscale’s Dogecoin Trust & 21Shares Polkadot ETF Signal New Era for Altcoins

Crypto.com Sets Ambitious Course: Cronos ETF and Stablecoin Launch in 2025

SEC Acknowledges Grayscale’s XRP & Dogecoin ETF Filings: A Game Changer or Regulatory Roadblock?

SEC Acknowledges Grayscale’s XRP & Dogecoin ETF Filings: A Game Changer or Regulatory Roadblock?

Total Unique Wallet Addresses of Each Blockchain and Growth Rate – September 2024 Report

Total Unique Wallet Addresses of Each Blockchain and Growth Rate – September 2024 Report

Market Capitalization to Revenue Ratio of Popular Layer 1 Blockchains: Where to Invest? Tron and Ethereum Lead the Pack

Market Capitalization to Revenue Ratio of Popular Layer 1 Blockchains: Where to Invest? Tron and Ethereum Lead the Pack

Ethereum’s Growth Surge in November 2024: Key Insights

The Explosion of Layer-2 Networks on Ethereum: Challenges and Opportunities

Liquid Staking on Ethereum Explodes — TVL to Explode From $284M to $17B by 2024

Ethereum’s Growth Surge in November 2024: Key Insights

The Explosion of Layer-2 Networks on Ethereum: Challenges and Opportunities

Liquid Staking on Ethereum Explodes — TVL to Explode From $284M to $17B by 2024

Record Crypto Trading Volumes on CEXs Hit All-Time High in December

Record Crypto Trading Volumes on CEXs Hit All-Time High in December

Trump’s World Liberty Financial Project Makes a Bold $48 Million ETH Purchase

Trump’s World Liberty Financial Project Makes a Bold $48 Million ETH Purchase

Ethereum Fee Earnings Increase in 2024 Despite Dencun Upgrade

Stablecoin Volume Surges Past Traditional Payment Giants (Visa & Mastercard): A Deep Dive into 2024’s Crypto Landscape

Ethereum Fee Earnings Increase in 2024 Despite Dencun Upgrade

Stablecoin Volume Surges Past Traditional Payment Giants (Visa & Mastercard): A Deep Dive into 2024’s Crypto Landscape

USDC Rebounds to $56.3 Billion Market Cap, Fully Recovering From Bear Market Losses

USDC Rebounds to $56.3 Billion Market Cap, Fully Recovering From Bear Market Losses

Ethereum Options Signal Potential Upside, But Risks Remain

Solana Shorts Surge: Are Memecoin Scandals Crashing the Party?

Ethereum Supply Squeeze: Exchange Reserves Plunge to 9-Year Low

Bitcoin Spot ETF liệu có giống Gold ETF trong quá khứ?

Tin BTC ETF tuần 03-09/06: Gần $2 tỷ chảy vào thị trường thông qua 10 quỹ Bitcoin ETF Mỹ

Ethereum Options Signal Potential Upside, But Risks Remain

Solana Shorts Surge: Are Memecoin Scandals Crashing the Party?

Ethereum Supply Squeeze: Exchange Reserves Plunge to 9-Year Low

Bitcoin Spot ETF liệu có giống Gold ETF trong quá khứ?

Tin BTC ETF tuần 03-09/06: Gần $2 tỷ chảy vào thị trường thông qua 10 quỹ Bitcoin ETF Mỹ

Financial Times: A Half-Baked Apology to the Bitcoin Community After 14 Years of Criticism

Financial Times: A Half-Baked Apology to the Bitcoin Community After 14 Years of Criticism

Why Japan is Not Ready to Include Bitcoin in Its National Reserves

Why Japan is Not Ready to Include Bitcoin in Its National Reserves