Key Takeaways:

- SEC cancels SAB 121, a rule that made custodied crypto liabilities of companies be recorded.

- The repeal was a success for the crypto industry and banks, which argued that SAB 121 was a barrier to growth.

- This signals a potential SEC shift towards clearer, innovation-focused crypto regulations.

Table of Contents

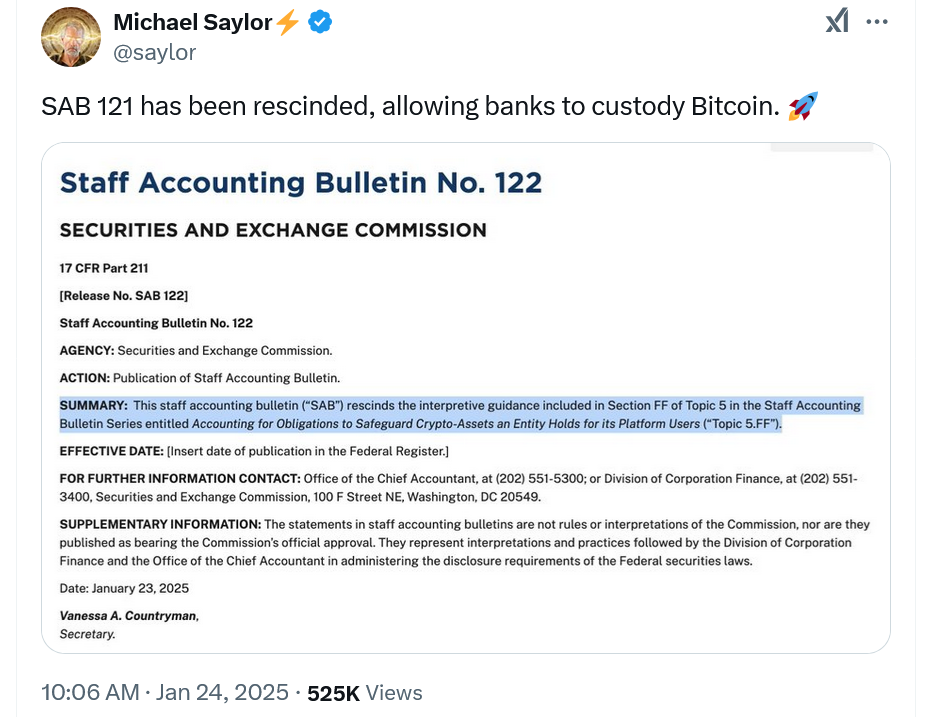

SEC Reverses Course: SAB 121 Crypto Accounting Rule Revoked

The Securities and Exchange Commission (SEC) has taken a significant step forward for the digital asset industry by officially repealing Staff Accounting Bulletin (SAB) 121. The nearly dismissed regulation, which defined how traditional financial companies should record cryptos on behalf of their customers, is a case of much dispute which the crypto industry as well as the conventional banking industry also criticized. The abolition of SAB 121 marks a crucial breakthrough, potentially signaling a new era in U.S. crypto regulation.

A Historical Context

The purpose of the origin of the SAB 121 rule by the SEC was to ensure the safety of the investments of the investors. The main reason was that in case of insolvency of a company that held crypto for clients, it was possible that they were not fully safeguarded and could be used as a compensation for the company’s creditors. This problem arose from the legal precedent that crypto assets may not always be “bankruptcy remote” i.e. separate from the company’s own assets.

Though this doubt is well-founded, SAB 121 was treated as an extremely widespread and standardized solution. The rule treated all custodied cryptocurrencies the same, regardless of the specific risks associated with them. The decline of entities such as FTX showed that the intermingling of customer funds and inadequate security were the glaring problems, but SAB 121 did not directly address these issues. Thus, it represented significant hurdles for the responsible crypto custody providers by imposing rules that didn’t actually solve the problems they were intended to?

What Was SAB 121 and Why Was it Controversial?

SAB 121 was introduced in March 2022 during the Gary Gensler regime and it mandated that financial institutions recording crypto assets of their customers should record them as liabilities on their balance sheets. This also implied that if a bank is holding let’s say 100 Bitcoin for its customers then it would have to show the same amount as a debt. (Its equivalent value as a debt)

This handling was thought by many to be very much wrong. Critics, like the company’s CEOs and sometimes the SEC members themselves, were arguing that this method didn’t reflect the reality of custody. It isn’t surrogate debt, after all. In fact, the property remains customer’s and is held on their behalf.

The Downside of SAB 121: A Closer Look

Under the rule, financial institutions and other entities regulated in the crypto area contended that SAB 121 created a remarkable threshold for these entities by way of regulation. The rescheduling of the balance sheet to list customer-holdings as liabilities by SAB 121 would lead to:

- Distortion of Financial Statements: The rule misleadingly blows up the number of liabilities on the balance sheet, thus leading to the subsequent presentation of very sick financial statements.

- Discourage the Development of Crypto Products: The extra accounting load and the resulting perceived risk could seriously deter traditional financial firms from offering crypto custody services, thus, innovation would be stifled.

- Enhancement of Risk Exposure: Exposing more assets held by various unregulated entities in light of the facts that the SAB 121 might make it difficult for the regulated entities to provide custody.

In addition, Representative Wiley Nickel said that SAB 121 would have had the effect of generating a “concentration risk by handing more control over to non-bank entities,” which are often not transparent and therefore easy to control. This becomes a real concern when it comes to the promotion of the broader adoption of cryptocurrencies exchange-traded products.

Industry Voices Celebrate the Repeal

The news about SAB 121 withdrawal has resulted in a favorable and positive reaction across the business and finance field. “Bye, bye SAB 121! It’s not been fun,” SEC Commissioner Hester Peirce tweeted on X, thus stating her joy for the rule’s repeal. Peirce, who has been one of the early and assertive detractors of SAB 121, was recently appointed as the leader of the new crypto task force in the SEC, signaling a more crypto-friendly approach of the commission.

X Legislator French Hill, who chairs the U.S. House of Representatives Financial Services Committee, also showed his approval, saying that he was “pleased” “to see the “misguided SAB 121 rule has been rescinded.” Quite the contrary, Hill claimed that “holding reserves against the assets held in custody is NOT standard financial services practice.” These are some of the highlights of his speech of the faulty nature of SAB 121, which did not heed the traditional financial principles.

The American Bankers Association expressed satisfaction with the repeal of SAB 121. As one of the institutions that had lobbied against the regulation, they welcomed the new regulatory approach. SAB 121 only limited their ability to develop and bring to market certain digital asset products and services, said ABA. This repeal will drive innovation and facilitate more access to regulated crypto custody solutions for consumers.

Michael Saylor also tweeted about this news.

A Shift in the Regulatory Tide?

The repeal of SAB 121 is the first major action led by Acting Chair Mark Uyeda, who previously served under the SEC during President Donald Trump’s administration. This is particularly notable given that a prior attempt to repeal the rule through a Congressional Review Act resolution faced a veto from former President Joe Biden. The House’s effort to override that veto fell short.

The change of opinion of the SEC so quickly under new leadership suggests a real turn in the commission’s way of operating with pieces of crypto tokens. Indeed, the new leadership within the SEC brings more observance in their administration and pushes innovation as they tread more cautiously on the investor’s side.

More News: SEC Forms Crypto Task Force Led by ‘Crypto Mom’ Hester Peirce – A Shift in Crypto Regulation

What Comes Next?

Even if the lifting of SAB 121 is an undeniable victory for the crypto industry, on the other hand, it is not the finalization of the regulatory argument. The SEC’s new team was entrusted with the creation of the more precise and comprehensive regulatory framework for the crypto assets. Acting Chairman Mark Uyeda himself stated that past handling of the topic resulted in “confusion about what is legal, which creates an environment hostile to innovation and conducive to fraud.” This suggests the focus moving forward will be on providing clarity and establishing clear rules, rather than relying on ad-hoc interpretive bulletins like SAB 121.

The new guidance will probably make companies follow rules established by the Financial Accounting Standards Board (FASB) or International Accounting Standard provisions. These are more traditional accounting principles. It’s important for entities to still “consider existing requirements to provide disclosures that allow investors to understand an entity’s obligation to safeguard crypto-assets held for others,” as the SEC noted in its recent bulletin. This means that while the accounting treatment is changing, the need for transparency remains paramount.

The removal of SAB 121 means a turning in crypto regulation in the United States. It suggests the readiness to hear out industry complaints and plans to foster a more conducive environment for the proper development of this segment which is exponentially growing. This bill is a part of promoting regulation in a way that will support the developments of innovation, clarity, and protection of investors.